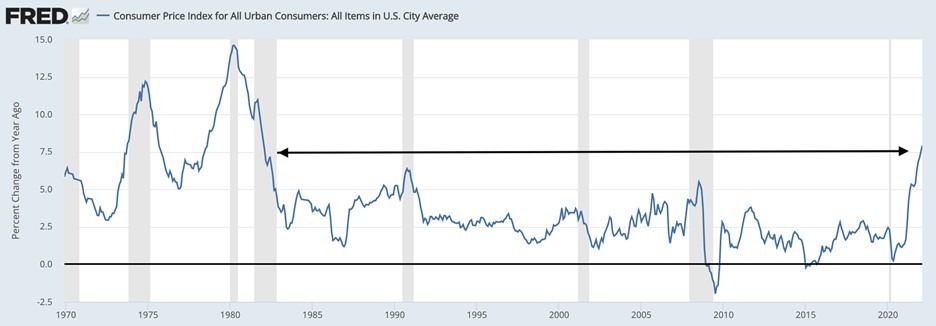

The most recent year-over-year Consumer Price Index (CPI) came in March 10th at 7.9% - the highest inflation reading since the early 1980s.

What are the chances that inflation continues much higher? What are the chances inflation moderates? How might that impact investors?

The case for higher inflation

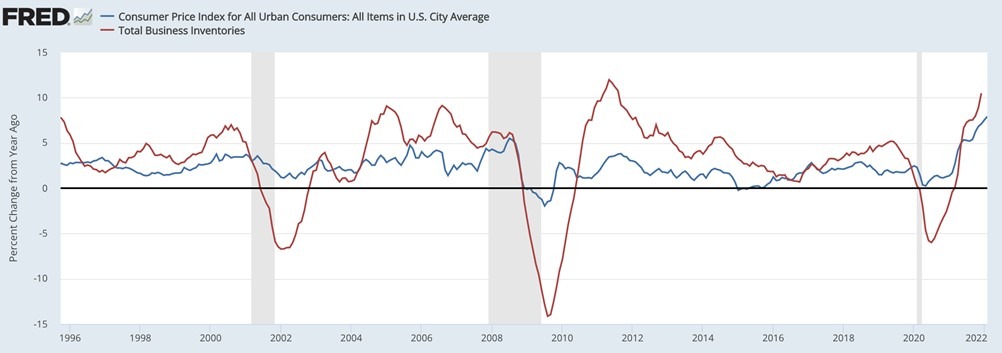

During the beginning of the pandemic, companies were not rebuilding inventories, so as the economy began to reopen and sales increased, companies got caught with fewer items in their warehouses to meet that demand. Today, we still have historically low inventories, and that leaves lots of room for businesses to continue to build. You can see from the chart below that Inventories (red) are a pretty good indicator of consumer prices (blue).

Throughout the month of March, we’ve seen an incredible run with most commodities. If prices remain elevated, you can expect the CPI to push higher. Wages often lead CPI and they have been very strong lately.

The case for moderating inflation

Inflation is represented by CPI and is measured year-over-year. In March of 2021, we had already seen readings rise significantly, so starting March of 2022, we will start to compare current prices to those that had already risen year-over-year. This means we should probably see lower readings throughout the rest of the year.

A big argument against continued elevated inflation is the slowing economy. The shipping index tends to track CPI pretty well, although the divergence can last a few months before they reconnect.

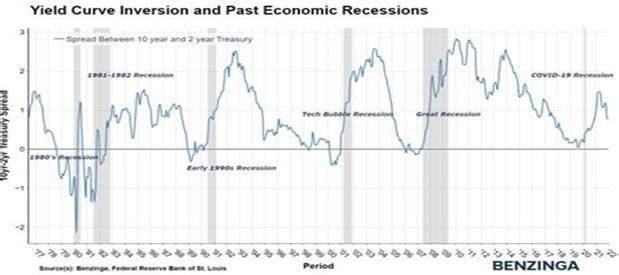

A flattening yield curve

On the chart above you can see that the yield curve was flattening both in ‘06 and ‘18. This is the type of environment that the Federal Reserve typically looks to “calm down” with monetary tightening, as the Central Bank does not want to be seen as contributing to an already weakening economic environment.

This could set the market’s tone for the next few months. Those banks that have been predicting 7 to 8 rate hikes in 2022 may begin to suggest that the Fed will run into trouble if they tighten too much. It may take a few rate hikes before the narrative really begins to shift and the markets price in easier monetary policy.

What this means to investors

So, we have some pretty strong arguments that inflation is still very much in play; however, year-over-year comparison may come more in line with historical readings because of the base effect and also may be helped by the slowing economy.

Although anything is possible, I believe it to be unlikely that the Fed begins to switch to a dovish tone before CPI has peaked. This may be for the May or June meeting, but investors are likely to “sniff it out” much earlier. This could trigger a large equity rally easily exceeding the all-time high (scenario mentioned above, would be similar to 2006 and 2018).

Until then, volatility is likely to remain elevated as investors continue to worry about future rate hikes.

Securities and advisory services offered through LPL Financial, a registered investment advisor. Member FINRA/SIPC.